- The R Roundup

- Posts

- Unveiling the Inflation Enigma: Navigating Economic Realities in 2024 and Beyond💵

Unveiling the Inflation Enigma: Navigating Economic Realities in 2024 and Beyond💵

We Bottomed...In Inflation🤔

Labyrinth Capital

February 03, 2024

As your weekend treat, RR is ringing you an insightful read from an expert in regards to macroeconomics with a spin on the crypto markets & the overall perception around Bitcoin ETFs

RR’s TL;DR🍿

The author believes that the current global economy is due for a downturn, and recent economic growth may not be sustainable🔻

They argue that the Reverse Repo Facility and QE have had a significant impact on the economy and could potentially cause inflation to reignite🔥

The author suggests that the FED may pivot to cut rates and possibly implement another round of QE to stimulate the economy🛑

Excited about a guest post?👀

Subscribe Before You Continue

Introduction

The global economy is growing faster than most expected, wildly, when many well-versed macroeconomists and investors were screaming for a recession and prolonged bear market. In 2024, inflation is under control, economic jobs are plentiful, and consumer households are resilient. But there is one side of the pond singing a different tune. They say the cost-of-living crisis is crippling many families as more living costs go towards revolving credit which currently charges record-high APRs. Consumers looking for new jobs say that the constantly positive reads by the governments are false and not reflective of the real economy. In their view, times are tight, but which narrative is more accurate?

Today, I will conduct a thorough macroeconomics article to help you understand precisely where the next quarter and months following could lead.

Could Inflation Reignite?

I have assessed the combined events over the past years, and it is my humble opinion that we have earned an overdue downturn in the global economy. In fact, before COVID-19 in 2019, we were heading for precisely that. We had a vast expansion driven by the low-interest rates, and this strange stimulus period in the form of Quantitative Easing altered the coming years, changing normal trends.

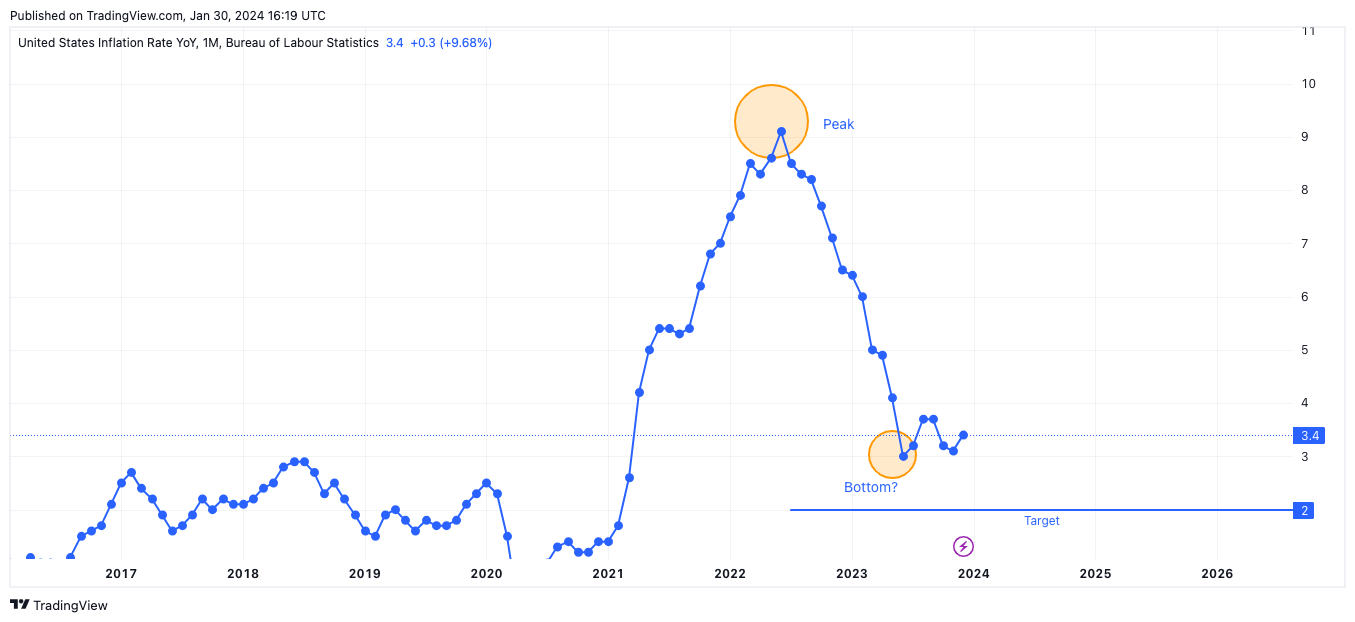

As we know, this resulted in inflation peaking at 9%, now dropping to 3.4%, and most believe we are now heading towards the FED's desired 2% target.

Inflation will remain sticky and bottomed at 2.9% in June 2023. Remember, it is currently at 3.4%.

If the global economy stays relatively upright as it has been since October 2023, we will not experience a hard or soft landing like the media likes to portray. Instead, there will be upward pressure on inflation as the economy hovers slowly to new highs, which will frustrate the idea that interest rates are coming down aggressively. On top of this, we have the Red Sea shipping lane issues, a lurking problem, and the rumours of QT (the opposite of QE) are grinding to a halt. So, if our thesis is correct and we have not quite proven to beat inflation, why is the market already pivoting to obscene rate cuts and the ending of QT? When the FED was performing QE, there was so much money in the system that would have kept interest rates forever at 0% that they instituted the reverse repo facility.

Reverse Repo Facility - What they don't tell you

I have been bashing on about this for so long, screaming from the rooftops that this facility is an EASING facility. During QE, if you were an institution with extra money, the FED, with their tools, provided the possibility for you to park your money at the Reverse Repo Facility, where they (FED) pay you 20bps below the top end of the Federal Funds Rate, currently 5.3% on top of your capital. The Reverse Repo Facility is a form of tightening. This is because the institutions (usually money market funds) place capital here at the FED instead of purchasing Janet Yellen’s T-Bills or Notes. This caused the uptick in bonds from the 2022 lows. Not purchasing T-bills removes liquidity from the financial system, and parking is at the FED. This capital is now OUTSIDE of the financial system.

Fast forward to 2024, and we are now getting hints from the FED that they will soon cut rates. As a result, what do you, as an institution with money at the reverse repo, do? You know that locking in a high rate of around 5.2% in a 6-month T-bill from Yellen is safer than waiting for rate cuts and earning less from the Reverse Repo Facility. So now that you’re buying T-bills again, all that sloshed-up money from the QE is flowing back into the financial system again.

We are now nearing the point where almost all the Reverse Repo facilities have been drained and have re-entered the economy, having peaked at $2.2. We are currently at $580bn and are around a month or two away from being empty. This facility being empty is a HUGE problem because it means that the Treasury will not have this excess money pit coming in. This means more bonds and notes will have to be issued over T-bills, which is why we have recently seen the 10Y spike around 4% over the past month. This is the primary concern: When the facility is empty, all we are left with is the FED doing QT and pulling liquidity out of the system. All things currently point towards a liquidity problem; the FED knows this. This is why rumours of tapering QT are being made known. Currently, the FED rolls over $95 billion a month. So, it is likely that this will begin to decrease as we near the full depletion of the Reverse Repo Facility.

The FED Is ALWAYS AHEAD

The FED knows that the oil for the engine in the financial system is liquidity. The system runs on overnight loans, obtaining overnight rates. If there is insufficient liquidity, there will be a vast disparity between what these same loans obtain in terms of higher rates, which would snowball and create further problems for the broader financial system. This is why QT will soon be reduced. The FED know that if they wait, unattended consequences could conspire. The drain of the Reverse Repo Facility is a form of easing that counteracts QT and the sting of rate hikes. So, whilst the FED is telling everyone that tightening is occurring, the market has shown the exact opposite. Once empty, the FED will want to prevent problems from occurring, hence the first-rate cut being speculated on by markets around March, the same time the facility is estimated to be empty.

Powell has avidly stated he has the tools to fix problems if something breaks. We saw this with the Bank Term Funding Program, where the FED stepped in and bailed out the regional banks. Now, I ponder if a premature pivot could reignite inflation again, which feeds into the narrative that we bottomed on inflation in June. The idea that the FED pivot, cut rates, possibly QE again, and stimulate the economy further is based on the idea that we are in the last legs towards the FED 2% inflation target. But what if we are not? And we end up reigniting inflation? It erases the FED's plan of cuts and QE, and the market is not ready for that conversation.

Why are markets so jubilant, then?

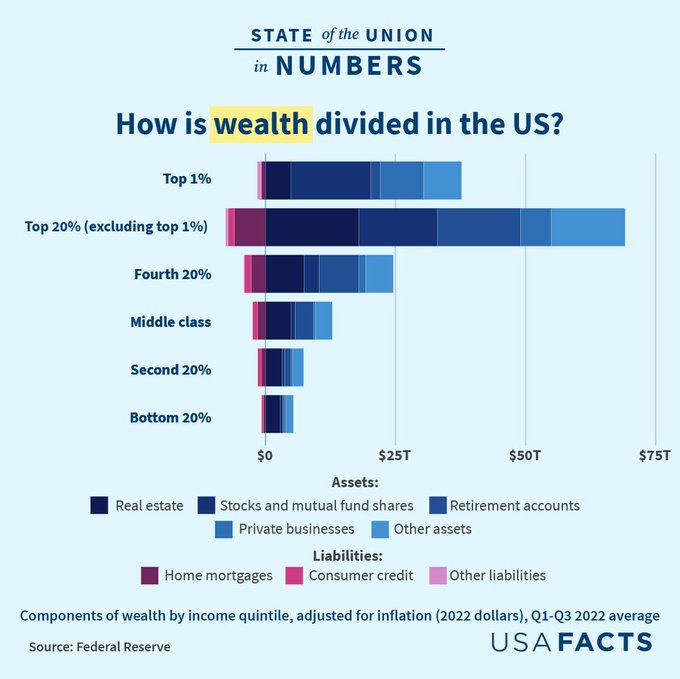

From an outsider’s perspective, the economies seem to be doing okay. After two years, we are back to slightly above trend, Bitcoin is hovering around $40k, and Gold is at all-time highs. Even though 2023 seemed a good year, a recent statistic that alarmed me is that the top 10% of households own 93% of the US's financial assets. From this alone, we get the notion that few people are spending, but rather, the top 10% are. Among those top 10% of individuals, interest rates have gone up as they have for everyone. Still, the difference between the rich and poor is that the rich have their financial position improved as they receive more interest income alone. The rising rates act as a stimulus on their net wealth.

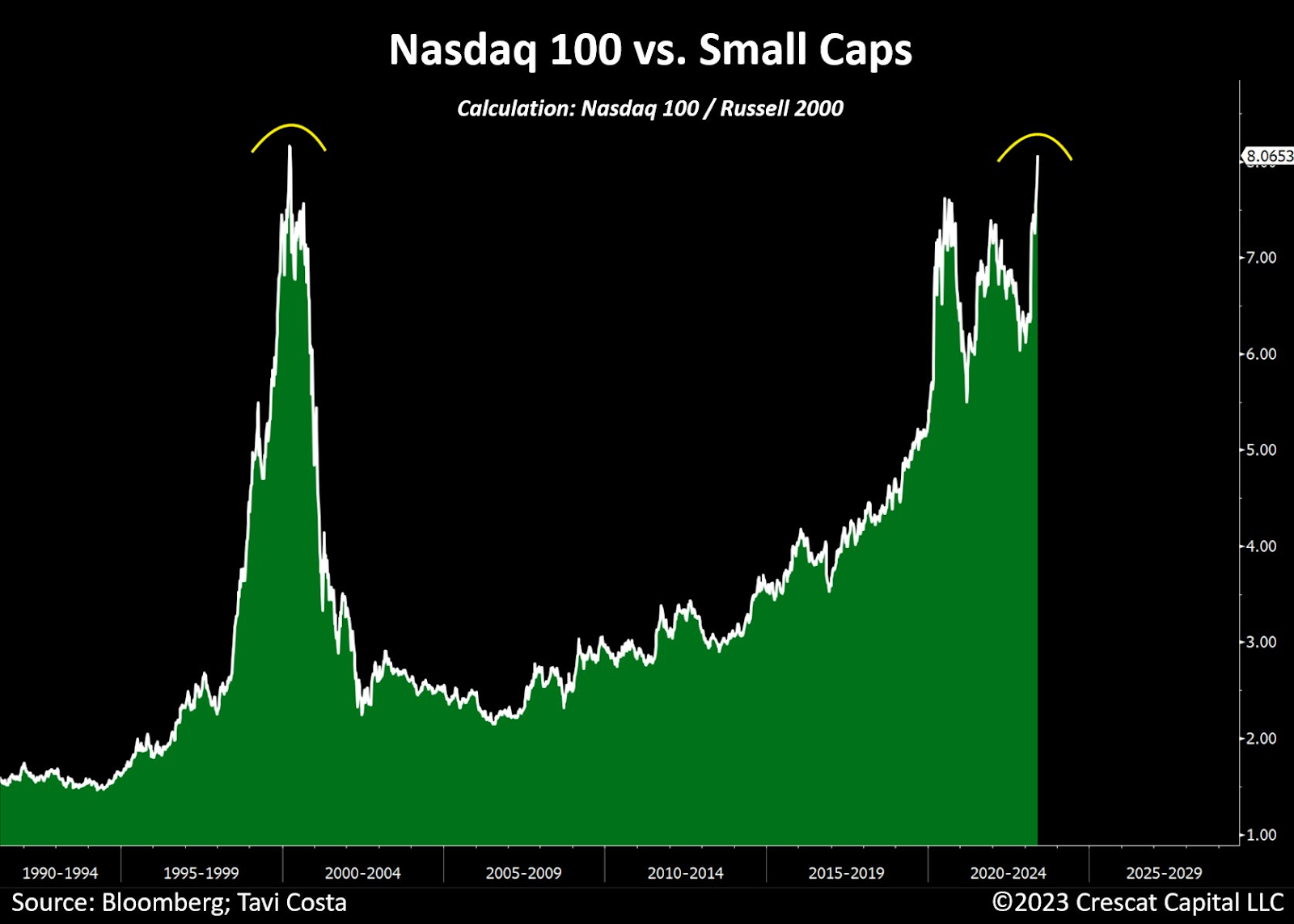

Concerning equities, it is likely we will see disappointment in economic data and, as a result, get lower revisions in earnings. Thinking about it retrospectively, we have double topped in broad markets, with NASDAQ and S&P500 being held up by seven stocks alone. This reflects a similar pattern experienced in the year 2000 cycle when we had a heavy retracement where the sentiment was that we would get to the end of the tightening cycle and then cuts would solve all the problems, but instead, they didn’t.

It wasn’t until a year later, in 2001 that there was a contraction in the economy. Stocks alone fell more than 50%. I am not saying this will happen again. However, we are back in the territory of EXTREME valuations. The love for tech has ballooned to levels last seen during the internet era. The AI craze, a significant contributor to the stock gains, fed into the bullish sentiment and speculative fever of the markets, which tells me we need to be cautious as investors.

COVID deformed the system to a great extent, a level that most of us cannot even fathom, and now a lot of the artificial intervention is being bled out of the system. We are now making our way back to where we were in 2019, except now, we have a system obsessed with cheap capital, facing higher capital costs and jacked interest rates, the highest since 2000. So, with all investors calling for a soft landing, you simply ignore the lag effect, implying that this time is different.

The Market Is On Crack

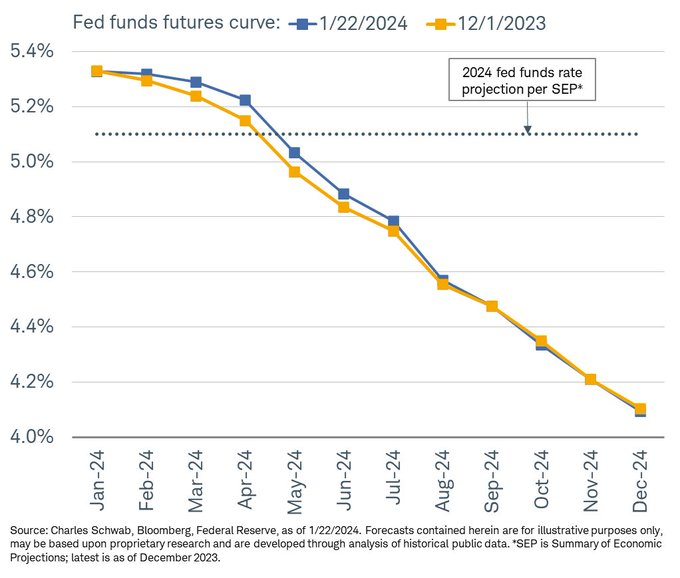

The funniest part about all this is that the market expects 7 rate cuts this year. Remember, there are only 8 meetings a year. So, the market expects a cut at every meeting. If the market is correct (and it never is), there are about 7 cuts; apart from being on immense crack, the only reason to cut this aggressively would be because the FED think the world ending.

Instead, the likelihood is that the FED cuts 3 times. However, this would still add fuel to the fire of reigniting inflation. Given that the 10% own 90% of the assets, lower rates would give them a reason to spend and increase capital investments. So now, in 2024, we are heading back towards the massive consumption phase after the stimulus has been exhausted and edging into the final contraction in the global economy. It is a well-known statistic that when the FED cut interest rates, although markets were seemingly jubilant about the FED pivot in 2024, history shows that it was only AFTER the rate cuts that we experienced the bulk of job losses. Only then is the worst part of the bear market in the picture, and the response to the problem is the FED cutting rates aggressively.

Bitcoin ETF – A Problem, Not a Solution

With crypto, I expect it to follow the trajectory of stocks, especially if sticky inflation persists. I still see cryptocurrency as the last line of inflows in a higher inflationary environment, which is ironic because it still gets coined as an inflation hedge. Unfortunately, I see Bitcoin following a similar trajectory to Gold's over the last few years. Gold used to be the ANTI FINANCIAL SOLUTION, and BTC, up until now, was also deemed just that, digital gold. The recent ETF news makes Bitcoin part of the problem, not the solution.

The ETF, as documented on the Labyrinth Capital Telegram Channel, was a clear buy-the-rumour sell-the-news event. Although I am bullish crypto long term, the ETF has roped the sector and community into believing centralisation is the future. This has diverted the attention from the ‘alternative financial system’ and ‘building in emerging economies’ and ‘helping the unbanked’ to gambling like a degen and to speculate like never before. The number of investors and crypto boys mesmerised by the ETF news is quite sad to see. If crypto can revert back to focus on building and not just looking at big numbers, then the sector can grow organically. I believe in this long term, but I expect downside before upside.

Conclusion

It’s important that we establish that as investors and traders we cannot afford to be backward-looking. Our thesis on the market must always be forward-looking as we assess the probabilities in the current world economy. Being too bearish or bullish can literally warp your perception and falter your investment strategy. We must acknowledge that what's changed about the economy post-pandemic is that there has been a huge attitude change towards spending. Inflation is sticky because the standard of living is so high that we immediately spend and invest. We are all guilty of it right? Money from your monthly checks come in and you don’t mind spending it on the new Tellytubby Coin which their marketing says will 100x in the next 3 days (I’m guilty and got rugged).

For now, this attitude hasn’t changed, we haven’t hit capitulation in my eyes. You will probably hear politicians, meme coin players and perma bulls telling you we are back to the euphoria stages of the bull market. I’m just here to say, when this sentiment comes back, this is when you want to be hedging your positions and taking a step back to reassess. Remember that bears become bulls when the fundamentals align!

Subscribe to the Labyrinth Capital Free Substack for stories like this👆

If you enjoyed this guest post, subscribe to our weekly newsletter for more👇

Reply